ECOMMERCE: Shingle signaled that it would soon be engaged in a pitched battle with Warby Parker to be the specialty-retail tastemaker to millennials. Each company has amassed dedicated fan bases who want a little meaning and a warm, do-gooder feeling packaged with their accessories. At the same time, both are expanding into new categories and new cities, pushing the boundaries of their brands. So whose vision of an authenticity-focused aspirational lifestyle is most attractive to people who believe that the soul of a company is as meaningful as its products?

ECOMMERCE: It was a pleasure to watch the company transition from a razor subscription service to a trusted men’s lifestyle brand, increasing margins each step of the way, and serving more than 3 million people. Many investors shy away from commerce companies. The multiples tend to be low, Amazon is ever-present, and lots of capital can be required to scale. To us, we didn’t see DSC as an “e-commerce” company, but instead as a model for new full-stack consumer products companies.

BROADBAND: The data suggest that Amazon could be in a great position as it tries to sell subscriptions to a bigger group of TV networks to compete with cable operators. Amazon has talked to media companies about terms of offering their channels, media executives say. It’s not known when or if Amazon might offer such a service. But media executives worry that Amazon, acting as a wholesaler of subscription services, could amass too much power by controlling access to customers without sharing much information with media firms.

BRAND: The maker of Tide detergent and Gillette razor blades was caught off guard by Dollar Shave Club's success, according to an article this week in the The Wall Street Journal, which cited anonymous sources. P&G's Gillette brand later launched its own online shave club, but not until 4 years later. Perhaps it's because P&G has been maniacally focused on slimming down its brand portfolio. That leaves less time and fewer resources to chase growth opportunities. After all, if the company's best deal folks are focused on selling off brands, then who is minding what's coming down the pike?

BRAND: Lack of differentiation, poor leadership, mediocre products, stale stories, misaligned market fit — these are some of the reasons businesses fail. But aside from that, many flounder because they simply fail to uphold a strong, meaningful brand. As the co-founder of Motto, an award-winning branding agency, I spend a lot of time helping leaders bring failing brands back from the brink of extinction. A phrase I hear often from brand leaders and CEOs is, “We rested on our laurels for too long.” Serena Williams ranks No. 1 in women’s tennis, but that doesn’t mean she doesn’t have to keep working for it.

ECOMMERCE: Indian ecommerce is a long-term game, likely to pan out for several years. To fight prolonged battles, especially against cash-rich behemoths like Amazon, Indian e-commerce companies require deep pockets. However, the sad truth is that they have not been able to raise the necessary capital in recent months and are in danger of losing out to Amazon, which has enough financial muscle to outlast local competition. Worse, Flipkart has had the ignominy of seeing its valuation being brought down by existing investors.

ECOMMERCE: Over the last few years, we've been very upfront about our love of lifestyle and accessories brand Cole Haan. The primary reason isn't just our appreciation for their technological advancements or design sensibilities, but the simpler statement that they look and feel good. JackThreads—who have demonstrated with their namesake label an equal dedication to craftsmanship and style, despite being relatively new—also shared this belief and the two have joined forces for a limited edition capsule collection.

MCOMMERCE: CustomInk is the nation’s 125th largest e-retailer with annual web sales of $273 million in 2015, according to the 2016 Top 500 Guide, and has grown at a compounded annual rate of 35% since 2011. CustomInk operates a pure responsive site in-house and forecasts its mobile sales to reach nearly $100 million this year. Responsive design is a format that adapts the look of a retail website to the device the consumer is using. It uses one code base, meaning retailers don’t have to operate several sites to account for the many types of screens consumers use to access the internet.

ECOMMERCE: Fashion eCommerce players now believe AI will give them a competitive edge above increasing automation and reducing costs. "If you look at fashion, personalised search is more through visuals than physical data like it is for electronic products. It is extremely critical for marketplaces like us to automate visual search through deep-learning technologies and we need to generate metadata automatically. It helps predict trends to stock up for particular occasions and also to eliminate duplicate products sold by multiple sellers on the platform in a customer's search."

DATA: As you probably have heard, Nintendo has partnered with game developer Niantic to launch a wildly popular game for iOS and Android called Pokémon GO. The game has already reached over 21M daily active users, dominated the in-game purchasing market, and players are spending more time in the game than on Facebook. It even stopped traffic in Central Park as players abandoned their cars to chase after a rare water Pokémon that had appeared in the vicinity.

ECOMMERCE: P&G is testing what it calls the Tide Wash Club, an online subscription service that ships its Tide Pods for free to shoppers. Shoppers can select the quantity and frequency that they receive the orders. Plans are oriented to shoppers who are single (P&G assumes they do about three loads a week), couples (five loads a week) and families (seven loads a week). For now, the test is limited to consumers in the Atlanta metropolitan area.

INNOVATION: In place of all the old V-8s, a grid of 18 massive cobalt blue boxes, each 10 feet high and 8 feet wide, now dominate the lab. They look a little like walk-in freezers, which isn’t too far off. They’re climate simulators, Nitz says as we file past row after row of them. Battery chemistry is fiendishly sensitive to temperature and humidity, he explains, and electric cars have to hold up in every kind of weather.

Last Word: On eCommerce Exits

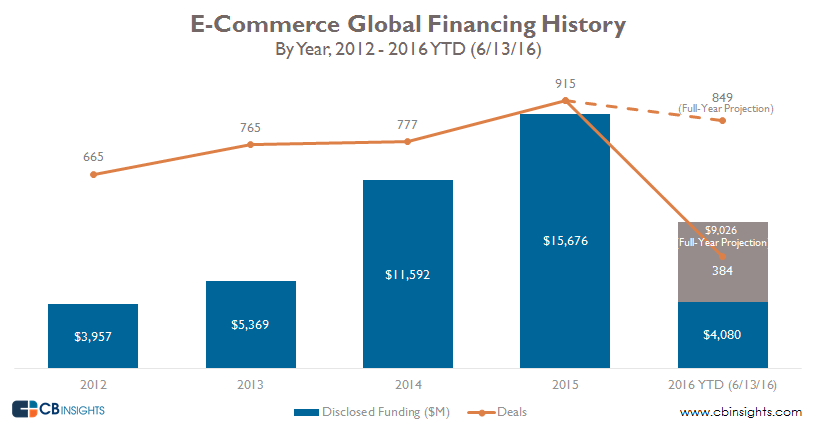

eCommerce financing is projected to land at a two year low in deals being done and a three year low in the aggregate price of those deals. Analysts have long communicated that this is indicative of a weakness in the eCommerce space but I've long sensed the opposite.

Over the last 12-16 quarters, Amazon has secured itself as the inevitable marketplace queen, venture and banking investments have been dispersed throughout exciting new fields like chat, AR and AI. And lastly, the sexiness of eCommerce has dwindled over the years due to unmitigated failures like FAB.com and that startup's affect on investors who were captivated by their inflated numbers and ease of fundraising.

By 2015, eCommerce was no longer a prime investment space. All the while, eCommerce operators have been functioning in ways that much of the rest of the startup community should have been imitating. Rather than optimizing for valuation (which Fab.com proved meant nothing), brands and platforms began optimizing for profitability. This, knowing that raising funds early stage capital would be more difficult.

In effect, eCommerce startups shrinked fundraising goals because cashflow was assisting their growth. To analysts that see deal size as strength, this would indicate a sector weakness. I've seen it as a strength. eCommerce founders have been aware of the laws of retail physics. Bigger deals meant fewer exit options.*

Over the next 4-6 quarters, zero sum eCommerce startup founders will begin to see exits again, especially in the consumer packaged goods and accessories spaces. Whether through acquisition by marketplaces like Flipkart, Alibaba, or Amazon. Or by incumbent brands who've been slow to achieve the same online footprint as their younger challengers. Dollar Shave Club's sensible success has opened the door for companies who have begun to achieve the same "niche" traction.

P&G paid $57B for 60% of the market when they purchased Gillette. Unilever just paid $1B for 15% of the same market. The economics are in the favor of both the acquirer and the acquired.

* 2015's aggregate deal size was greatly impacted by Jet.com's funding, which I cannot defend.

![Amazon a Surprise Force in Internet TV [ACCESS FOR THE FIRST 30 CLICKS]](https://goodbits-production.s3.amazonaws.com/uploads/link/thumbnail/3596876/be79cc9c-a61d-4212-b32a-c5a3b2b652af.jpg)